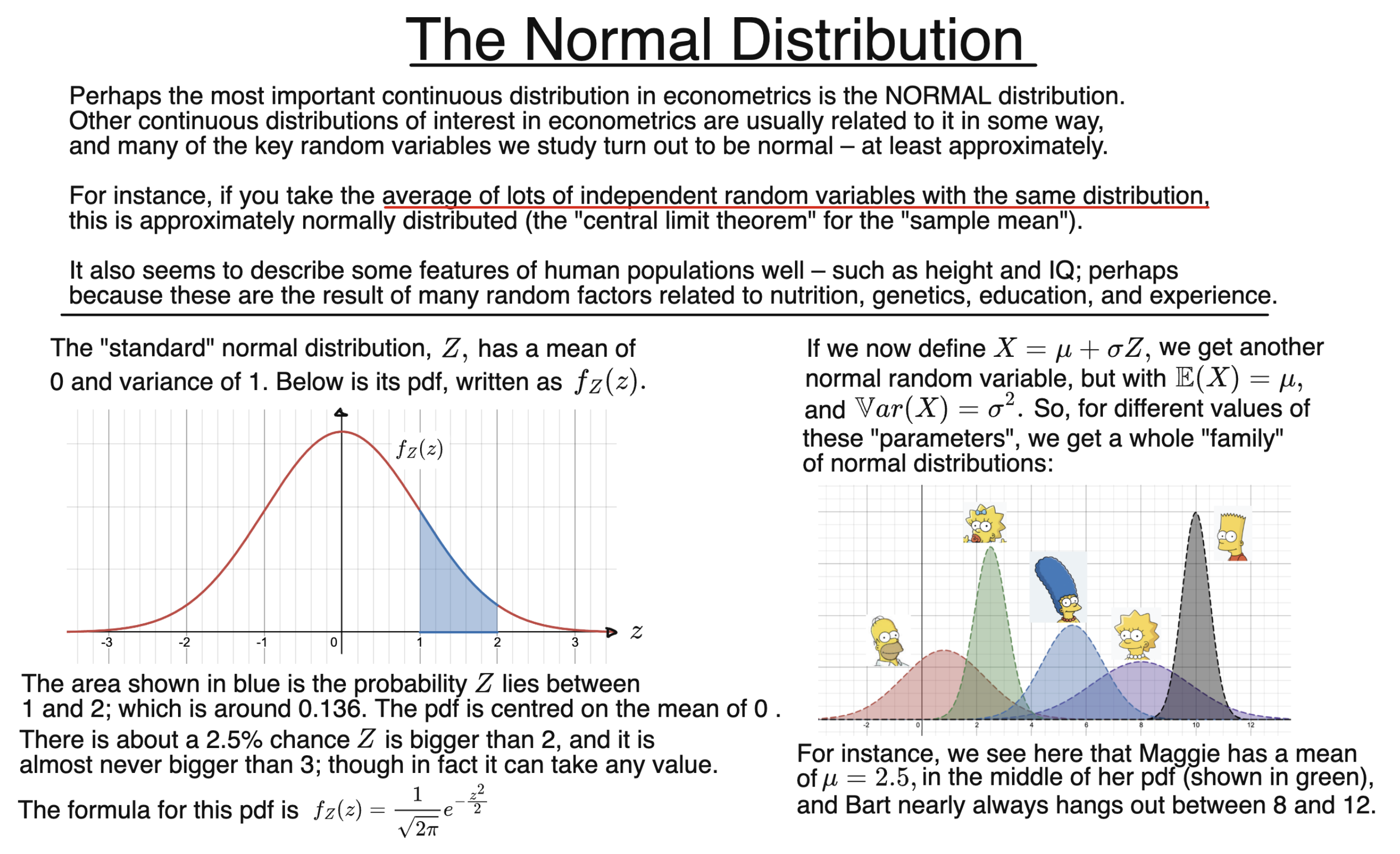

What is a Normal Distribution?

A random variable with a normal distribution is continuous, and can in principle take any value. A normal distribution has two “parameters”:

– its mean, $\mu$, which for normal random variables is also the highest point of the PDF (the mode), and:

– its variance, $\sigma^2$. The larger this is, the more “spread out” around the mean the distribution is.

Changing these numbers affects the “personality” of the random variable, and alters the shape of the PDF.

The PDF is always symmetric around the mean, so half of the area is to the left of this point, which is therefore also the median. It is often called a “bell curve” because of its distinctive shape. The larger the variance, the more spread out the curve becomes.

Many real-life random variables can be modelled well by a normal distribution. Examples include data on human heights, weights, and IQ.

Moreover, it turns out that many random quantities of interest in statistics and econometrics have a normal distribution; at least approximately – for instance, the “sample mean”, a random variable of great importance in statistics.

The particular case when $\mu=0$ and $\sigma^2=1$ is called the standard normal distribution. This is especially important, and is used to define other, more complex continuous distributions – in particular, the chi-squared, t-, and F-distributions.

| Notation: | $X \sim \mathcal{N}(\mu,\sigma^2)$ |

| Type: | $ \text{Continuous} $ |

| PDF: | $ f_X(x) = \frac{1}{\sqrt{2\pi}\sigma}e^{-\frac{(x-\mu)^2}{2\sigma^2}} $ |

| Support: | $x \in \mathbb{R} $ |

| Mean: | $\mathbb{E}(X) = \mu $ |

| Variance: | $\mathbb{V}\text{ar}(X) = \sigma^2 $ |