What is a Moment?

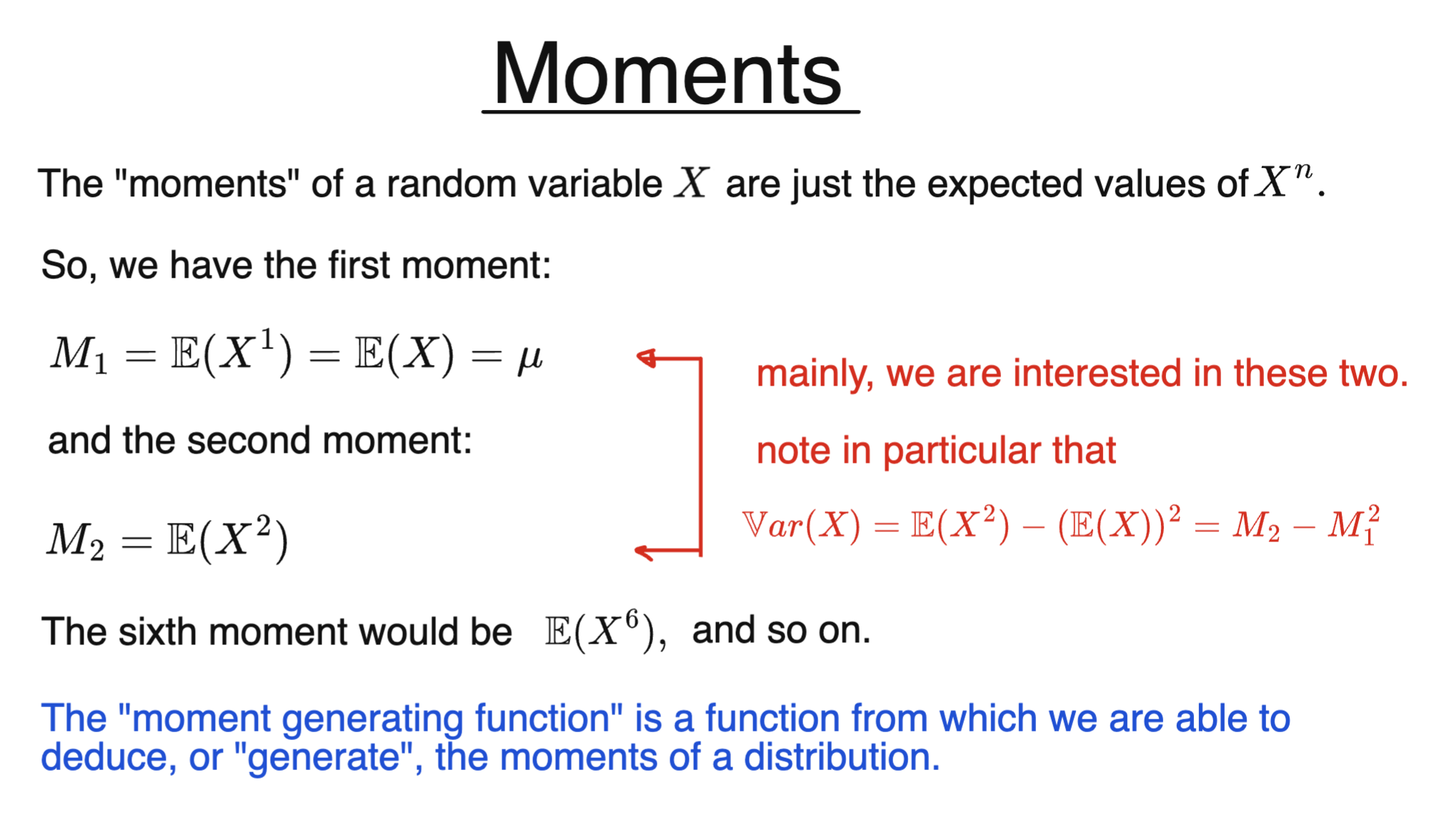

For a random variable $X$, its moments are just the expected values of its powers; that is, $\mathbb{E}(X^n)$, for each value of $n$.

We can write $M_n$ for the $n^{th}$ moment of $X$. Note that $M_n$ is just a number, not a function or a random variable.

If $n=1$, we get the mean:

$$M_1(X)=\mathbb{E}(X)$$

The formula for the variance, meanwhile, involves both the first and second moment:

$$\mathbb{V}\text{ar}(X) =\mathbb{E}(X^2) - \left(\mathbb{E}(X)\right)^2 =M_2-(M_1)^2$$

In statistics and econometrics, we are mainly interested in these two moments.

The third moment, $\mathbb{E}(X^3)$, relates to the skewness of a distribution. The fourth moment, $\mathbb{E}(X^4)$, refers to how “fat” the “tails” of a distribution are; if it is large, this signifies that “extreme” events are more probable.

One way to find moments is by using a “moment generating function”.